Tax Increment Financing

What Is Tax Increment Financing?Tax Increment Financing (TIF) is a tool utilized by municipalities throughout the country to finance public improvements in identified areas of need, known as a redevelopment district or Downtown Development Authority (DDA). TIF can be implemented through the creation of a DDA.

A DDA can provide public amenities that encourage and facilitate corresponding “new development” within an approved geographic district. For example, a DDA might use funds generated from a new development or a redevelopment to participate in the financing for new streetscapes, plazas, sidewalks, streets or simply to improve traffic/pedestrian circulation that would help to make the new development possible.

A DDA can also provide assistance to existing property owners who might want to rehabilitate or expand their property. An example of this might be a Public Improvement Reimbursement Agreement. This financing tool is not new and has been utilized around the country for decades to help fund public improvements and encourage redevelopment.

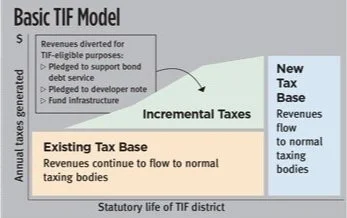

How does TIF work?PROPERTY TAX: Once a DDA is established and a Plan of Development is adopted, the property tax base for the district is frozen. This means that after the date of the plan adoption, the assessed value to which the mill levy for the City, the school district, the county and other taxing jurisdictions would be the same each year thereafter with adjustment only for general reassessments (which occurs every odd year).

For example, if the assessed value of property in the district increases to $10 million in year 5 of the plan, the taxes derived from multiplying the combined mill levy times the $1 million base go to the overlapping taxing jurisdictions and the mill levy times the $9 million increase would go to the DDA. So revenues that would have ended up with the county and other entities through increases in tax revenues tied to redevelopment, stay in the City and more specifically, in the DDA.

SALES TAX: The plan can also affect City sales tax revenue, but not state or county sales tax revenues. The plan can dedicate sales tax revenues above the base year revenues to the DDA.

Once these revenues are captured, this new stream of revenue can be utilized to pay debt service on bonds that can be issued by the City (DDA) for public improvements. Bonding may be necessary, as it would typically take a period of time to acquire enough revenue to fund public improvements.

Lending institutes find TIF a very stable source of revenue and therefore readily lend money when secured by TIF. Bonds are only put in place once construction of public improvements begins and assuming the DDA has the financial capacity to repay the debt. TIF can be utilized for up to 25 years from the date of establishment.

Is TIF a new tax?NO. No new taxes are established using TIF nor are taxes (either property tax or sales tax) increased. The revenues produced by increased property values and increased retail sales activity are simply redistributed to benefit the DDA for public improvements in the district.

This graph generally depicts how TIF revenues are captured by the DDA.Click here for more information about our TIF policy and program requirements.